Treasury Yields, Oil Prices, and International Tensions

January 2, 2024

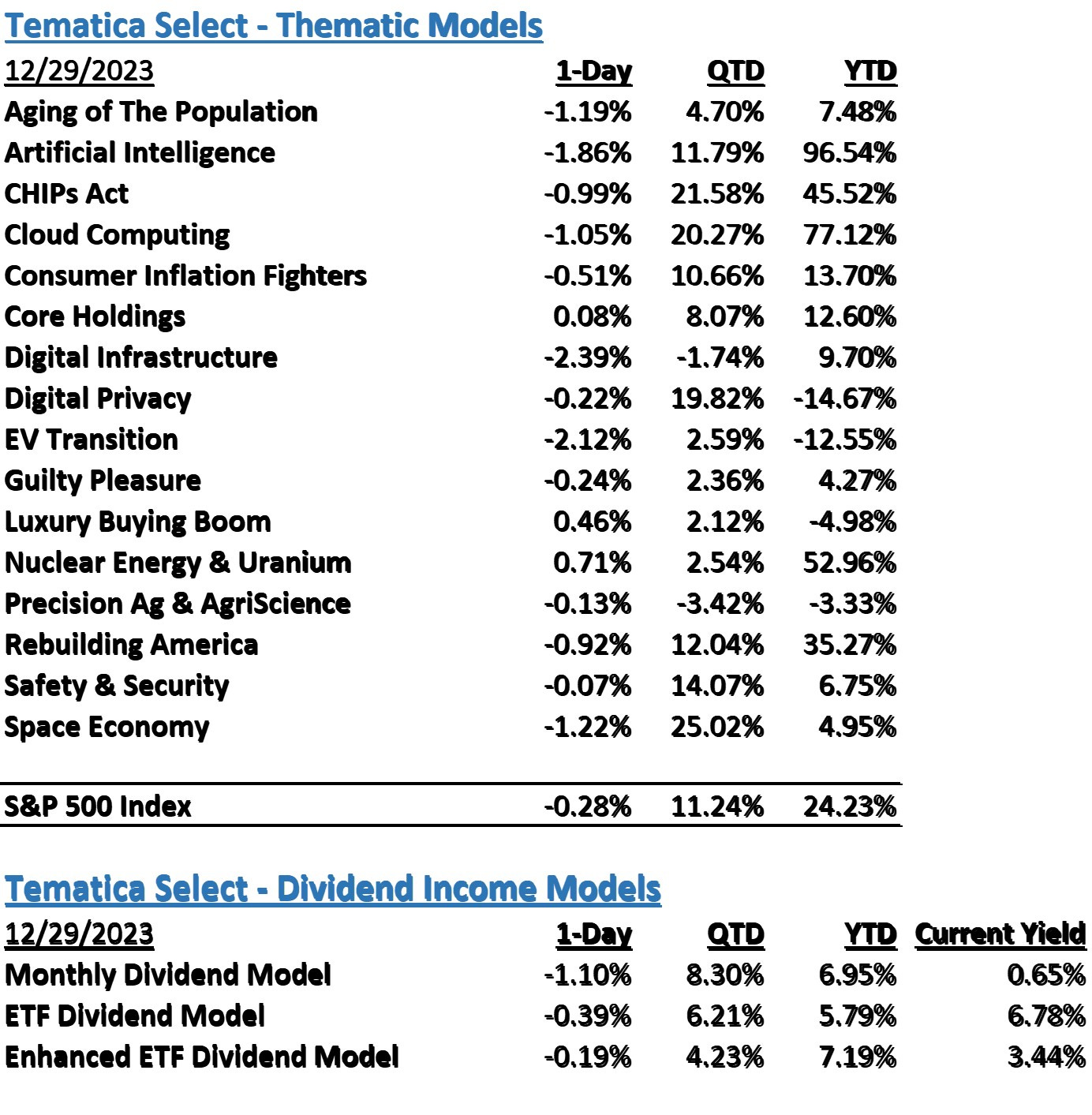

Equities closed out 2023 with a bit of a whimper as the Dow came close to flat, down 0.05%, the S&P 500 fell 0.28%, the Nasdaq Composite dropped 0.56% and the Russell 2000 closed 1.52% lower. Despite Friday’s lackluster performance, last year saw broad indexes, not to mention what we’ll call mature crypto assets post impressive numbers as indicated below:

Dow Jones Industrial Average: 13.70%

S&P 500: 24.23%

Nasdaq Composite: 43.42%

Russell 2000: 15.09%

Bitcoin (BTC-USD): 152.97%

Ether (ETH-USD): 91.57%

If there was a topic of conversation, it was the persistent narrowness of the participation that drove these returns. We all have heard that the so-called “Magnificent Seven” dragged markets higher, but those seven stocks were distributed only among three sectors. Given the sector proxies’ 2023 returns shown below, can you figure out which are the homes of those seven names?

Energy Select Sector SPDR Fund (XLE): -4.15%

Financial Select Sector SPDR Fund (XLF): 9.94%

Consumer Staples Select Sector SPDR Fund (XLP): -3.38%

Utilities Select Sector SPDR Fund (XLU): -10.17%

Industrial Select Sector SPDR Fund (XLI): 16.07%

Health Care Select Sector SPDR Fund (XLV): 0.39%

Materials Select Sector SPDR Fund (XLB): 10.12%

Technology Select Sector SPDR Fund (XLK): 54.68%

Communication Services Select Sector SPDR Fund (XLC): 51.41%

Real Estate Select Sector SPDR Fund (XLRE): 8.48%

Consumer Discretionary Select Sector SPDR Fund (XLY): 38.44%

Getting back to Friday’s results, in individual names, Boston Scientific (BSX) rose 2.72% on reports that the company expects a new atrial fibrillation platform to gain FDA approval in the coming quarter.

Treasury Yields, Oil Prices, and International Tensions

US equity futures point to a down market open to start the new trading year. Investors are optimistic for 2024 spurred on by potential rate cuts, cooling inflation, an earnings rebound, and sector diversification outside of the “Magnificent Seven” that sent the S&P 500 and Nasdaq Composite soaring last year and erased 2022 losses. In the short-term, after rocketing 15%-20% higher during the last few months of 2023 those market barometers, from a technical perspective, are flirting with overbought territory as other indicators are looking exhausted. Investor sentiment measured by the Fear & Greed Index continues to flash “Extreme Greed” while the latest AAII Investor Sentiment Index saw a rebound in Bearishness during the last week of the year.

That mindset is contending with renewed hostility between Ukraine and Russia, Israel indicates its war will continue for “many months”, and both oil prices and Treasury yields rebounding. Following such a sharp run in the market, a pullback could be in the cards, and that would give investors, especially those who missed out on the November-December market run, an opportunity to put capital to work at better prices.

For more, be sure to read our Daily Markets column published each day by Nasdaq.

The strategies behind our Thematic Models:

Aging of the Population - Capturing the demographic wave of the aging population and the changing demands it brings with it.

Artificial Intelligence – Software, chips, and related companies that facilitate the collection and analysis of large data sets and autonomous generation of solutions given non-machine language prompts.

CHIPs Act – Capturing the reshoring of the US semiconductor industry and the $52.7 billion poised to be spent on semiconductor manufacturing.

Cloud Computing – Companies that provide hardware and services that enhance the cloud computing experience for users, such as co-location, security, and edge computing.

Consumer Inflation Fighters - Companies poised to benefit as consumers stretch the disposable spending dollars they do have.

Core Holdings – Companies that reflect economic activity and are large enough to not get pushed around by day-to-day market trends. Low-beta, large-cap names able to better withstand economic turmoil.

Digital Infrastructure & Connectivity -The buildout and upgrading of our Networks, Data Storage Facilities, and Equipment.

Data Privacy & Digital Identity - Companies providing the tools and services that verify authorized users and safeguard personal data privacy.

EV Transition - Capturing the transition to EVs and related infrastructure from combustion engine vehicles.

Guilty Pleasure – Companies that produce/provide food and drink products that consumers tend to enjoy regardless of the economic environment and potential long-term health hazards associated with excessive consumption.

Nuclear Energy & Uranium – Companies that either build and maintain nuclear power plants or are involved in the production of uranium.

Luxury Buying Boom - Tapping into aspirational buying and affluent buyers amid rising global wealth.

Precision Ag & Agri Science – Companies that look to address shrinking arable land by helping maximize crop yields utilizing technology, science, or both.

Rebuilding America - Turning the focused spending on rebuilding US infrastructure into revenue and profits.

Safety & Security – Targeted exposure to companies that provide goods and services primarily to the Defense and security sectors of the economy.

Space Economy – Companies that focus on the launch and operation of satellite networks.

The strategies behind our Dividend Income Models:

Monthly Dividend Model – Pretty much what the name says – this model invests in companies that pay monthly dividends to shareholders.

ETF Dividend Model – High-yielding ETFs that provide a range of exposures from domestic equities, international equities, emerging market equities, MLPS, and REITs.

ETF Enhanced Dividend Model – A group of high-yielding ETFs that utilize options to enhance yield through collecting option income.