The Week Ahead: Inflation Data, Fed Speakers, Two Big Conferences, and Bank Earnings Begin

January 8, 2024

Last week was a sobering experience for the stock market as December PMI, job creation, and wage data showed the economy remains stronger than expected, pushing back on the market’s expectation for six rate cuts in 2024. Our view has been we could see 2-4 rate cuts beginning in late 2Q 2024 with the bulk of them coming in 2H 2024. We are seeing more folks get on board with that thinking.

Readers should shake off the last of their New Year blues because the coming week will be a rapid-fire assault of sorts with highly anticipated inflation data, Fed speakers, bank earnings, and attention-getting conferences. The outcome of those events will determine if the market rebounds or continues last week’s move lower. Jumpstarting the week, oil prices are lower following news Saudi Arabia will cut key crude prices for buyers in all regions for February. That is in addition to its voluntary product cuts of 2 million barrels per day through 1Q 2024.

Economic Data

On the economic front, we have a combination of Fed speakers and December inflation data, and following last week, we can safely say investors and traders alike will be laser-focused on both. Coming off last week's economic data that pushed back hard on the market's expectation for six rate cuts this year, we strongly suspect Fed speakers on Monday and Wednesday will reiterate the Fed is in no rush to begin cutting rates this year. Thursday and Friday bring the December CPI and PPI reports, respectively, and we will need to see considerable progress in the data, especially the December core CPI data, to elicit a more dovish stance from the Fed. That will put Friday's comments from Minneapolis Fed President Neel Kashkari in the spotlight.

Earnings

This coming week sees a trickle of corporate earnings before the December quarter deluge kicks off on Friday with the usual early earnings cycle group of bank earnings. Quarterly results from Jefferies (JEF) will be a barometer of December quarter investment banking activity, but its comments about IPO and deal activity will be of far more interest. With Albertsons (ACI), we're looking for confirmation consumers at more at home during the holiday season, but we'll also be curious about what it says about inflation bubbling through its supply chain. Similarly, with results from KB Home (KBH), we'll be interested in whether the company saw a pickup in housing demand as mortgage rates fell and what that means for new home construction in the quarters ahead.

As we hinted at, Friday brings bank earnings from several companies, including Bank of America (BAC), JPMorgan Chase (JPM), Citigroup (C), and Wells Fargo (WFC). Across that group of earnings reports, the market will size up comments on loan activity, net interest income, sales, and trading as well as investment banking activity. Also on Friday, Delta Air Lines (DAL) will report its December quarter results, which should benefit from falling fuel costs as well as robust air travel trends.

Later today, the 26th Annual ICR Conference will kick off and run through January 10 with more than 250 public and private companies presenting. The conference continues to have a retail-facing bent with notable presentations from Darden Restaurants (DRI), Dutch Bros (BROS), First Watch Restaurants (FWRG), J. Jill (JILL), Urban Outfitters (URBN), and Walmart (WMT). Coming off the holiday shopping season, management comments about revenue trends and input costs will be top of mind for investors as they prepare for the December quarter earnings season and reassess 2024 consensus EPS expectations for the S&P 500.

From Tuesday, January 9 through the end of the week, CES 2024 will be held, and this annual showcase of new products and technologies will generate ample headlines. The expectation is artificial intelligence will be front and center with Nvidia’s (NVDA) expected to showcase several new GPUs at the event and AMD (AMD) is also expected to make several announcements. Companies participating in keynote speeches include Siemens (SIEGY), L’Oréal (LRLCY), Snap (SNAP) McDonald’s (MCD), Walmart, Intel (INTC), Elevance Health (ELV), Microsoft (MSFT), Qualcomm (QCOM), and Best Buy (BBY).

As both conferences are held, readers should be on alert for earnings pre-announcements that could either send a company’s shares soaring or result in a far less desirable outcome.

For more, be sure to read our Daily Markets column published each day by Nasdaq.

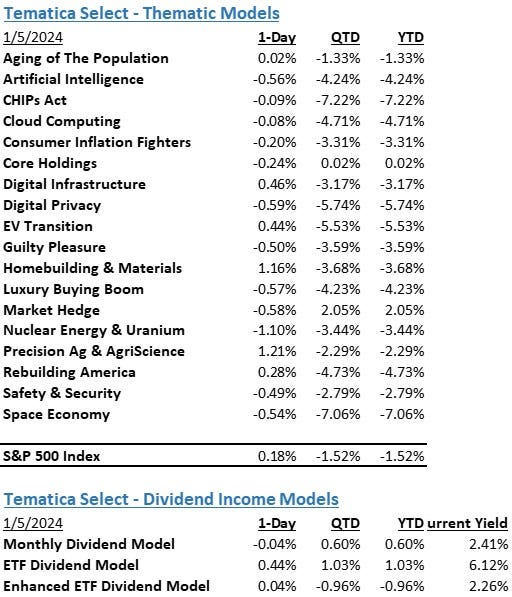

The strategies behind our Thematic Models:

Aging of the Population - Capturing the demographic wave of the aging population and the changing demands it brings with it.

Artificial Intelligence – Software, chips, and related companies that facilitate the collection and analysis of large data sets and autonomous generation of solutions given non-machine language prompts.

CHIPs Act – Capturing the reshoring of the US semiconductor industry and the $52.7 billion poised to be spent on semiconductor manufacturing.

Cloud Computing – Companies that provide hardware and services that enhance the cloud computing experience for users, such as co-location, security, and edge computing.

Consumer Inflation Fighters - Companies poised to benefit as consumers stretch the disposable spending dollars they do have.

Core Holdings – Companies that reflect economic activity and are large enough to not get pushed around by day-to-day market trends. Low-beta, large-cap names able to better withstand economic turmoil.

Digital Infrastructure & Connectivity -The buildout and upgrading of our Networks, Data Storage Facilities, and Equipment.

Data Privacy & Digital Identity - Companies providing the tools and services that verify authorized users and safeguard personal data privacy.

EV Transition - Capturing the transition to EVs and related infrastructure from combustion engine vehicles.

Guilty Pleasure – Companies that produce/provide food and drink products that consumers tend to enjoy regardless of the economic environment and potential long-term health hazards associated with excessive consumption.

Homebuilding & Materials – Ranging from homebuilders to key building product companies that serve the housing market, this model looks to capture the rising demand for housing, one that should benefit as the Fed returns monetary policy to more normalized levels.

Luxury Buying Boom - Tapping into aspirational buying and affluent buyers amid rising global wealth.Market Hedge Model – This basket of daily reset swap-based broad market inverse ETFs protects in the face of market pullbacks, overbought market technicals, and other drivers of market volatility.

Nuclear Energy & Uranium – Companies that either build and maintain nuclear power plants or are involved in the production of uranium.

Precision Ag & Agri Science – Companies that look to address shrinking arable land by helping maximize crop yields utilizing technology, science, or both.

Rebuilding America - Turning the focused spending on rebuilding US infrastructure into revenue and profits.

Safety & Security – Targeted exposure to companies that provide goods and services primarily to the Defense and security sectors of the economy.

Space Economy – Companies that focus on the launch and operation of satellite networks.

The strategies behind our Dividend Income Models:

Monthly Dividend Model – Pretty much what the name says – this model invests in companies that pay monthly dividends to shareholders.

ETF Dividend Model – High-yielding ETFs that provide a range of exposures from domestic equities, international equities, emerging market equities, MLPS, and REITs.

ETF Enhanced Dividend Model – A group of high-yielding ETFs that utilize options to enhance yield through collecting option income.