The Week Ahead

Mobile World Congress - Another AI frenzy in the making (see today's Model Musings)

Last week was another strong week for the market, which was propelled higher by blowout quarterly results and guidance from AI darling Nvidia (NVDA). As we work towards the end of February and the beginning of the final month of the March quarter, these final days of February kick off with Mobile World Congress 2024, an event that will be filled with new product announcements and service announcements. We expect it will be another showcase for AI-related headlines as companies remind investors AI is more than just Nvidia.

The pace of quarterly earnings continues to abate, but still, there will be some insights on food inflation and corporate spending that investors will want to contemplate. The week’s economic data brings fresh insights into inflation and the speed of the economy. Mixed with several Fed speakers sprinkled throughout the week, rate cut expectations could be pushed out further if the January core PCE price index mimics other January inflation figures, coming in above market expectations.

Earnings

While corporate earnings are winding down the week has an ample number of cybersecurity companies reporting. Their results and guidance will reveal if last week’s disappointing report from Palo Alto Networks (PANW) was a company-specific issue or the result of a more widespread slowdown in corporate spending. Comments from Salesforce (CRM), Snowflake (SNOW), HP (HPQ), and Hewlett Packard Enterprises (HPE) about that and AI will be top priorities this week.

The other big insight this week will be on food inflation and the prospects for improving food prices. Insights on both will be collected when Domino’s Pizza (DPZ), JM Smucker (SJM), Hormel Foods (HRL), Papa John's (PZZA), and Utz Brands (UTZ) report.

On the consumer front, we have Best Buy (BBY), TJX Companies (TJX), and Inter Parfums (IPAR)reporting while those watching construction and homebuilding activity will want to dial into results from Trex (TREX) and TopBuild (BLD) but also Redfin (RDFN).

Economic Data

Coming off of last Thursday's Flash February PMI reports from S&P Global and getting ready for the usual start of the new month data, we will be focused on the February Manufacturing PMI data from ISM as well as the final version for S&P Global's (SPGI) January Manufacturing PMI. Key areas of interest will be input and output costs, new orders, and employment as we get ready to receive February data for the CPI and PPI as well as the next Employment Report. In other words, the next set of must-watch data when it comes to the Fed and potential rate cuts.

Adding another dimension to that will be the January PCE Price Index that arrives alongside the January Personal Income & Spending data. We should see further evidence that real wage growth has returned but given the upside surprises found in the January CPI and PPI data, the market will be scrutinizing the January core PCE index very closely and how it stacks up against the 2.9% year-over-year print for December. Currently, the Cleveland Fed's Inflation Nowcasting model pegs the January figure at 2.74% vs. the 2.8% market consensus.

While it is increasingly in the rearview mirror, we will parse the second print for 4Q 2023 GDP, comparing it to the initial reading of 4.9%. We suspect that figure will be revised somewhat lower, and we'll be interested to see what, if any, revisions were made for 4Q 2023 PCE Price Index data.

For more, be sure to read our Daily Markets column published each day by Nasdaq.

Model Musings

Artificial Intelligence

“Qualcomm, at the Mobile World Congress 2024, has announced over 75 new large language models optimised for the Snapdragon platform. The company has also confirmed that some of these models will be powering generative AI capabilities across next-generation smartphones, PCs, IoT, XR devices, and software-defined vehicles.” Read more here

“ServiceNow (NYSE: NOW), the leading digital workflow company making the world work better for everyone, and NVIDIA (NASDAQ: NVDA) today announced that they are broadening their relationship with the introduction of telco-specific generative AI solutions to elevate service experiences. The first solution, Now Assist for Telecommunications Service Management (TSM), is built on the Now Platform and uses NVIDIA AI to help boost agent productivity, speed time to resolution, and enhance customer experiences.” Read more here

“Google announced a new set of features for phones, cars, and wearables — using Gemini to craft messages, AI-generated captions for images, summarizing texts through AI for Android Auto, along with access to passes on Wear OS.” Read more here

“FWD Group Holdings Limited (“FWD Group” or “FWD”) today announced it is extending its partnership with Microsoft with a four-year agreement to provide access to the latest generative artificial intelligence (AI) innovations, while continuing to support FWD’s cloud-first technology strategy. FWD Group plans to drive its generative AI initiatives by leveraging Microsoft’s Azure OpenAI Service and other enterprise-grade innovations. FWD Group expects to benefit from the private networking, monitoring and security capabilities of Microsoft Azure as well as its advanced AI models.” Read more here

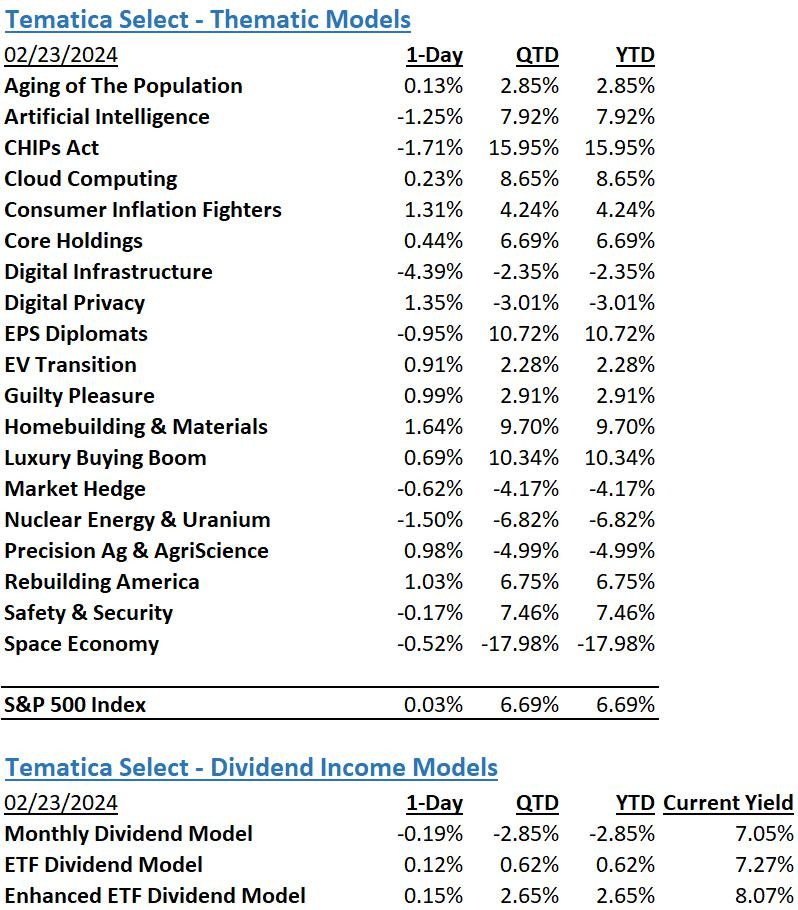

The Strategies Behind Our Thematic Models

Aging of the Population - Capturing the demographic wave of the aging population and the changing demands it brings with it.

Artificial Intelligence – Software, chips, and related companies that facilitate the collection and analysis of large data sets and autonomous generation of solutions given non-machine language prompts.

CHIPs Act – Capturing the reshoring of the US semiconductor industry and the $52.7 billion poised to be spent on semiconductor manufacturing.

Cloud Computing – Companies that provide hardware and services that enhance the cloud computing experience for users, such as co-location, security, and edge computing.

Consumer Inflation Fighters - Companies poised to benefit as consumers stretch the disposable spending dollars they do have.

Core Holdings – Companies that reflect economic activity and are large enough to not get pushed around by day-to-day market trends. Low-beta, large-cap names able to better withstand economic turmoil.

Digital Infrastructure & Connectivity -The buildout and upgrading of our Networks, Data Storage Facilities, and Equipment.

Data Privacy & Digital Identity - Companies providing the tools and services that verify authorized users and safeguard personal data privacy.

EPS Diplomats - Profitable large capitalization companies proven to produce above-average EPS growth and provide investors with the benefit of multiple expansion.

EV Transition - Capturing the transition to EVs and related infrastructure from combustion engine vehicles.

Guilty Pleasure – Companies that produce/provide food and drink products that consumers tend to enjoy regardless of the economic environment and potential long-term health hazards associated with excessive consumption.

Homebuilding & Materials – Ranging from homebuilders to key building product companies that serve the housing market, this model looks to capture the rising demand for housing, one that should benefit as the Fed returns monetary policy to more normalized levels.

Market Hedge Model – This basket of daily reset swap-based broad market inverse ETFs protects in the face of market pullbacks, overbought market technicals, and other drivers of market volatility.

Luxury Buying Boom - Tapping into aspirational buying and affluent buyers amid rising global wealth.Market Hedge Model – This basket of daily reset swap-based broad market inverse ETFs protects in the face of market pullbacks, overbought market technicals, and other drivers of market volatility.

Nuclear Energy & Uranium – Companies that either build and maintain nuclear power plants or are involved in the production of uranium.

Precision Ag & Agri Science – Companies that look to address shrinking arable land by helping maximize crop yields utilizing technology, science, or both.

Rebuilding America - Turning the focused spending on rebuilding US infrastructure into revenue and profits.

Safety & Security – Targeted exposure to companies that provide goods and services primarily to the Defense and security sectors of the economy.

Space Economy – Companies that focus on the launch and operation of satellite networks.

The strategies behind our Dividend Income Models:

Monthly Dividend Model – Pretty much what the name says – this model invests in companies that pay monthly dividends to shareholders.

ETF Dividend Model – High-yielding ETFs that provide a range of exposures from domestic equities, international equities, emerging market equities, MLPS, and REITs.

ETF Enhanced Dividend Model – A group of high-yielding ETFs that utilize options to enhance yield through collecting option income.

Don’t be a stranger

Thanks for reading and if you have a suggestion for an article or book we should read, or a stream we should catch, email us at info@tematicaresearch.com. The same email works if you want to know more about our thematic and targeted exposure models listed below.