The Week Ahead

Goldman ups its S&P 500 target again; earnings from retailers and Nvidia

Except for the small-cap heavy Russell 2000, last week saw the other major market indices give back varying degrees of year-to-date gains. Even with that modest setback, through the first half of the first quarter of 2024, the S&P 500 was up 4.9% and the Nasdaq Composite 5.1%. Coming into this week, investor sentiment remains at “Extreme Greed” even though both of those market barometers moved further away last week from being overbought.

As we move into the next phase of the current earning season, which will focus on retail-facing companies, Goldman Sachs (GS) once again lifted its target for the S&P 500, this time to 5,200, in part spurred by their continuing belief that the Fed is on track for 5 rate cuts. In November, the firm’s target was 4,700 and in December it boosted its forecast to 5,100.

Underpinning its latest increase is a more optimistic outlook for earnings for the basket, which now sits at $241 for this year and $256 in 2025, up from $237 and $250 previously. Those revisions reflect expectations for “stronger economic growth and higher profits” for the information technology and communication-services sectors, which include Magnificent Seven companies Apple (AAPL), Microsoft (MSFT), Nvidia (NVDA), Alphabet (GOOGL), and Meta Platforms (META). What stands out, however, is Goldman not calling for additional multiple expansion, which means its target hinges on companies continuing to lift bottom-line expectations over the coming quarters. Nvidia reports after Wednesday’s market close - see below for more on what the market expects.

Economic Data

We have another abbreviated trading week coming up and as you can see below it will be light on economic data. Our focus will be on two reports: the January Fed meeting minutes and the February Flash PMI data from S&P Global.

Inside the Fed meeting minutes, we'll be looking for clues about how quickly the central bank could move to cut rates. But given the recent spate of inflation data, those minutes and their insights may not be all that insightful.

We'll be looking at the Flash February PMI data for indications about the economy’s ability to continue to grow above trend. The January Flash and Final PMI provided valuable insight that helped us identify the risk of the higher-than-expected January CPI and PPI prints, which came to pass last week. That will have us closely parsing this week's Flash February PMI data similarly. With gas prices up ~6% compared to this time last month, per data from AAA, there are reasons to think the inflation commentary could support a continuing sticky view on inflation.

Outside of those two reports, given this week's inflation data and what it showed, we will be tuning into comments from Atlanta Fed President Raphael Bostic on Tuesday, and Philly Fed President Patrick Harker and Minneapolis Fed President Neel Kashkari who are both scheduled to speak on Wednesday. As it stands now, we do not see them wavering from an increasingly patient attitude toward rate cuts given the mounting number of data pointing to inflation being stickier than expected.

Earnings

Just under 80% of the S&P 500 basket have reported their quarterly results surprising to the upside. The next push of earnings reports skews toward retailers and for that, the bar has been set by the trailing three-month data found in the January Retail Sales report. Total retail-only sales during the November to January period rose 2.2% year over year, and that figure will be the yardstick that measures quarterly results this week from Walmart (WMT).

Quarterly results from Dutch Bros (BROS), Cheesecake Factory (CAKE), and Wingstop (WING) will be sized up against the 9.3% year-over-year gain for restaurant sales found in the same report. And for Home Depot (HD) the market will be eyeing the 4.9% year-over-year fall in Building Materials retail sales but also what the company has to say about the current April quarter especially given expectations for early spring weather this year.

Outside of retailers, because of the performance impact it has had on the S&P 500 as well as the Nasdaq Composite, quarterly earnings from Nvidia (NVDA) will be in the spotlight this week. While Amazon (AMZN), Alphabet (GOOGL), Meta (META), and Microsoft (MSFT) have all upped their spending on AI and related support technologies, including data center, the 2024 consensus EPS forecast for Nvidia calls for $21.19, up significantly from the $11.65 booked in 2023. Should the company’s guidance underwhelm Wall Street, its shares, which account for 4.24% of the S&P 500 and 5.25% of the Nasdaq Composite, have the potential to weigh on those market benchmarks. Given the more than 50% move in Nvidia shares over the last seven weeks, it’s fair to say expectations for its earnings and guidance are running high.

For more, be sure to read our Daily Markets column published each day by Nasdaq.

Model Musings

Artificial Intelligence

AI is driving massive demand for edge computing infrastructure, as industrial and commercial users need to process more data locally to take advantage of AI's capabilities… Hardware and software providers alike are concluding that edge computing — moving processing power closer to where data is being generated — provides a bridge between 5G networks and cloud data centers. They're starting to package all three services.” Read more here

“U.S. software giant Microsoft (MSFT.O), opens new tab will expand its artificial intelligence (AI) and cloud infrastructure in Spain through an investment of $2.1 billion in the next two years, the company's Vice Chair and President Brad Smith said in a post on social media site X. The move comes on the heels of its announcement of a 3.2 billion euros ($3.45 billion) AI-focused investment in Germany, spanning the next two years.” Read more here

CHIPs Act

"The US plans to award $1.5 billion to GlobalFoundries, the largest domestic maker of made-to-order semiconductors, as part of the Biden administration’s effort to strengthen the nation’s chip production. The funding, outlined in a non-binding preliminary agreement, would flow to three projects: a new fabrication facility in Malta, New York, the expansion of an existing site in Malta and expansion of its Burlington, Vermont, manufacturing site. The US is also offering the company $1.6 billion in federal loans." Read more here

Luxury Buying Boom

“Chinese shoppers have increasingly turned to Hainan in recent years as three years of pandemic-related border closings cut off the option of purchasing beauty brands such as L'Oreal-owned Lancome and Estee Lauder's La Mer at duty free counters in Korea or Hong Kong. Global luxury players, including brands from leading conglomerates LVMH, and Kering also piled into Hainan to reach consumers domestically. The expansion of Hainan's duty-free shopping in 2025 also means luxury brands can operate their own duty-free stores, rather than rely on partnerships with local players such as China Duty Free Group.” Read more here

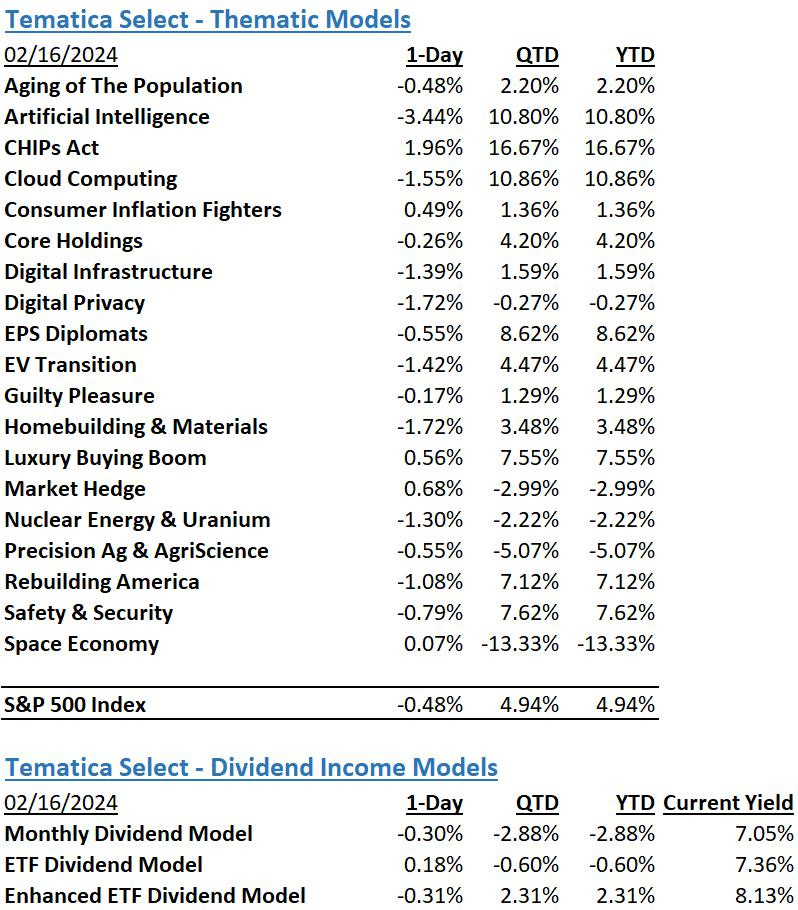

The Strategies Behind Our Thematic Models

Aging of the Population - Capturing the demographic wave of the aging population and the changing demands it brings with it.

Artificial Intelligence – Software, chips, and related companies that facilitate the collection and analysis of large data sets and autonomous generation of solutions given non-machine language prompts.

CHIPs Act – Capturing the reshoring of the US semiconductor industry and the $52.7 billion poised to be spent on semiconductor manufacturing.

Cloud Computing – Companies that provide hardware and services that enhance the cloud computing experience for users, such as co-location, security, and edge computing.

Consumer Inflation Fighters - Companies poised to benefit as consumers stretch the disposable spending dollars they do have.

Core Holdings – Companies that reflect economic activity and are large enough to not get pushed around by day-to-day market trends. Low-beta, large-cap names able to better withstand economic turmoil.

Digital Infrastructure & Connectivity -The buildout and upgrading of our Networks, Data Storage Facilities, and Equipment.

Data Privacy & Digital Identity - Companies providing the tools and services that verify authorized users and safeguard personal data privacy.

EPS Diplomats - Profitable large capitalization companies proven to produce above-average EPS growth and provide investors with the benefit of multiple expansion.

EV Transition - Capturing the transition to EVs and related infrastructure from combustion engine vehicles.

Guilty Pleasure – Companies that produce/provide food and drink products that consumers tend to enjoy regardless of the economic environment and potential long-term health hazards associated with excessive consumption.

Homebuilding & Materials – Ranging from homebuilders to key building product companies that serve the housing market, this model looks to capture the rising demand for housing, one that should benefit as the Fed returns monetary policy to more normalized levels.

Market Hedge Model – This basket of daily reset swap-based broad market inverse ETFs protects in the face of market pullbacks, overbought market technicals, and other drivers of market volatility.

Luxury Buying Boom - Tapping into aspirational buying and affluent buyers amid rising global wealth.Market Hedge Model – This basket of daily reset swap-based broad market inverse ETFs protects in the face of market pullbacks, overbought market technicals, and other drivers of market volatility.

Nuclear Energy & Uranium – Companies that either build and maintain nuclear power plants or are involved in the production of uranium.

Precision Ag & Agri Science – Companies that look to address shrinking arable land by helping maximize crop yields utilizing technology, science, or both.

Rebuilding America - Turning the focused spending on rebuilding US infrastructure into revenue and profits.

Safety & Security – Targeted exposure to companies that provide goods and services primarily to the Defense and security sectors of the economy.

Space Economy – Companies that focus on the launch and operation of satellite networks.

The strategies behind our Dividend Income Models:

Monthly Dividend Model – Pretty much what the name says – this model invests in companies that pay monthly dividends to shareholders.

ETF Dividend Model – High-yielding ETFs that provide a range of exposures from domestic equities, international equities, emerging market equities, MLPS, and REITs.

ETF Enhanced Dividend Model – A group of high-yielding ETFs that utilize options to enhance yield through collecting option income.

Don’t be a stranger

Thanks for reading and if you have a suggestion for an article or book we should read, or a stream we should catch, email us at info@tematicaresearch.com. The same email works if you want to know more about our thematic and targeted exposure models listed below.