Stocks Look To Claw Back Recent Losses, But…

Today's Atlanta Fed GDPNow model update, 2H 2024 S&P 500 EPS prospects in focus

Following the worst day of trading in US stocks in almost two years, equity futures suggest the market will attempt to reclaim some of that lost ground today. Lending a helping hand is the pronounced reversal in Japan’s Nikkei 225, which finished up more than 10% earlier today following yesterday’s yen “carry trade” drop of 12.4%.

While yesterday’s better than expected July Service PMI reports from ISM and S&P Global helped walk back investors from the recession ledge after last week’s disappointing July Employment Report and July Manufacturing PMI data, we have little in the way of fresh economic data today. One often overlooked data set, the US Logistics Manager’s Index increased to 56.5 in July, the highest in four months, compared to 55.3 in June, and marking eight consecutive months of expansion in the logistics sector.

The US Logistics’ Manager’s data also showed Transportation Prices hit the highest since May of 2022, making it the third consecutive month in which prices moved higher due to tight capacity and increasing demand. Survey respondents are predicting that these dynamics will hold, suggesting that the freight recession is waning. That pricing data follows the upward trend in July Service PMI pricing components, suggesting further progress on inflation could be on the slow path.

As this gets baked into investor thinking, we’ll be following today’s update for the Atlanta Fed’s rolling GDP forecast, better known as its GDPNow Model. The last figure put 3Q 2024 GDP at 2.5%, but that was before the July jobs report and yesterday’s Service PMI data for July. The likelihood is we see today’s GDPNow revision move lower, but the question is how much lower compared to the initial GDP print of 2.8% for 2Q 2024? A big drop could stoke renewed concerns of a hard landing for the economy, but before we jump the gun let’s remember this is a rolling forecast that is updated as new economic data is published. Meaning we will see a wide array of inputs ahead of the Fed’s next policy meeting that concludes in 43 days.

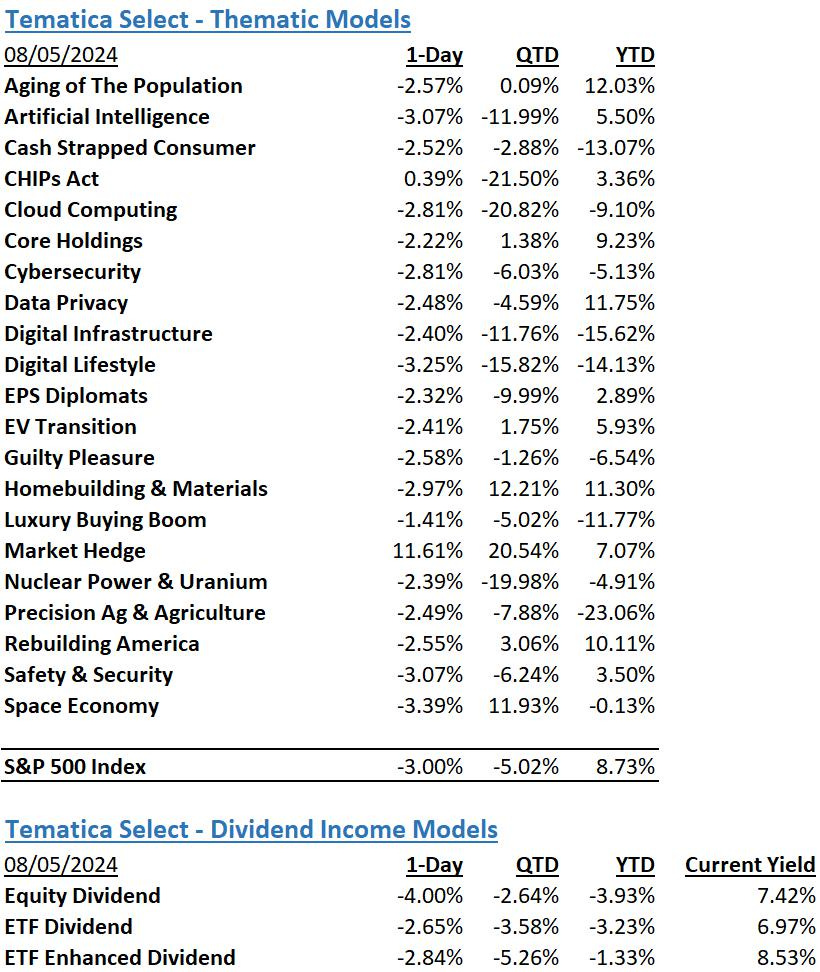

The coming days also bring earnings reports from the last 25% of the S&P 500 basket. So far EPS expectations for that market barometer have inched up for 2Q 2024, but those for 2H 2024 have slipped to 8.8% compared to more than 11% just a few weeks ago per data compiled by FactSet. With reports of increasingly selective consumers, which supports our Cash-Strapped Consumer model, earnings from consumer facing companies could lead that 2H 2024 EPS consensus forecast even lower. This suggests that even though the market is looking to claw back some of its recent losses, we may have a bit further to go until we are out of the proverbial woods. That could give readers a continued reason to contemplate our Market Hedge model.

Model Musings

Artificial Intelligence

“Our growth across the commercial and government markets has been driven by an unrelenting wave of demand from customers for artificial intelligence systems that go beyond the merely performative and academic. The large language models that have transfixed the world will only be capable of transforming the work of a multinational business or a defense agency’s operations if their power is unleashed within the context of an enterprise software system that has an opinionated view of the world—its idiosyncratic objects, logic, and physics.” Read more here

Artificial Intelligence, Digital Infrastructure

“Lumen Technologies (NYSE: LUMN) today announced it has secured $5 billion in new business driven by major demand for connectivity fueled by AI. Large companies across industry sectors are seeking to secure fiber capacity quickly, as this resource becomes increasingly valuable and potentially limited, due to booming AI needs. In addition, Lumen is in active discussions with customers to secure another $7 billion in sales opportunities to meet the increased customer demand.” Read more here

Digital Infrastructure

“The banking industry is experiencing a seismic shift as agile, digital-native FinTechs capture an ever-growing share of the market. Burdened by outdated technology, traditional financial institutions face mounting challenges in delivering modern digital services. The growing dominance of FinTechs — securing nearly half of all new account openings — highlights the urgency for banks to modernize their infrastructure.” Read more here

“I did do some attribution analysis, on XLRE, which is our proxy for the real estate sector. And 60% of that 2.8% return can be attributed to three specialty REITs and the specialty they are in is data center and transmission. Digital infrastructure, right?” Watch More Here

Market Hedge

“A rapid unloading of “carry trades” extended on Monday, with market participants seeking to roll back on the popular strategy amid a dramatic global sell-off in risk assets… I think all of these things that people typically had on expecting a more quiet period and now we’ve got everything but. That’s the thing to watch out for,” he added.“ Read More Here

“The Monday morning peak was the highest level the VIX has hit since March 2020, shortly after the Federal Reserve’s emergency actions during the Covid-19 pandemic, according to FactSet. The VIX rose as high as 85.47 in March 2020, according to FactSet.“ Read More Here

Nuclear Power & Uranium

“Nuclear power is the second-largest source of low carbon energy used today to produce electricity, following hydropower. During operation, nuclear power plants produce almost no greenhouse gas emissions. According to the IEA, the use of nuclear power has reduced carbon dioxide emissions by more than 60 gigatonnes over the past 50 years, which is almost two years’ worth of global energy-related emissions.“ Read More Here

“Two technologies could greatly extend the uranium supply itself. Neither is economical now, but both could be in the future if the price of uranium increases substantially. First, the extraction of uranium from seawater would make available 4.5 billion metric tons of uranium—a 60,000-year supply at present rates.“ Read More Here

“… in 2022, the 2,700 U.S. data centers consumed around 4% of the country's total electricity generated electricity, according to the International Energy Agency. The agency projects that by 2026, such centers will make up 6% of electricity use. Many technology companies are investing in or partnering with nuclear power providers to ensure energy supplies for their data centers.” Read more here

The Strategies Behind Our Thematic Models

Aging of the Population - Capturing the demographic wave of the aging population and the changing demands it brings with it.

Artificial Intelligence – Software, chips, and related companies that facilitate the collection and analysis of large data sets and autonomous generation of solutions given non-machine language prompts.

Cash Strapped Consumer - Companies poised to benefit as consumers stretch the disposable spending dollars they do have.CHIPs Act – Capturing the reshoring of the US semiconductor industry and the $52.7 billion poised to be spent on semiconductor manufacturing.

Cloud Computing – Companies that provide hardware and services that enhance the cloud computing experience for users, such as co-location, security, and edge computing.

Core Holdings – Companies that reflect economic activity and are large enough to not get pushed around by day-to-day market trends. Low-beta, large-cap names able to better withstand economic turmoil.

Cybersecurity - Companies that focus on protecting against the penetration of digital networks and the theft, ransom, corruption or destruction of data.

Digital Infrastructure & Connectivity -The buildout and upgrading of our Networks, Data Storage Facilities, and Equipment.

Digital Lifestyle - The companies behind our increasingly connected lives.

Data Privacy & Digital Identity - Companies providing the tools and services that verify authorized users and safeguard personal data privacy.

EPS Diplomats - Profitable large capitalization companies proven to produce above-average EPS growth and provide investors with the benefit of multiple expansion.

EV Transition - Capturing the transition to EVs and related infrastructure from combustion engine vehicles.

Guilty Pleasure – Companies that produce/provide food and drink products that consumers tend to enjoy regardless of the economic environment and potential long-term health hazards associated with excessive consumption.

Homebuilding & Materials – Ranging from homebuilders to key building product companies that serve the housing market, this model looks to capture the rising demand for housing, one that should benefit as the Fed returns monetary policy to more normalized levels.

Luxury Buying Boom - Tapping into aspirational buying and affluent buyers amid rising global wealth.

Market Hedge Model – This basket of daily reset swap-based broad market inverse ETFs protects in the face of market pullbacks, overbought market technicals, and other drivers of market volatility.

Nuclear Energy & Uranium – Companies that either build and maintain nuclear power plants or are involved in the production of uranium.

Precision Ag & Agri Science – Companies that look to address shrinking arable land by helping maximize crop yields utilizing technology, science, or both.

Rebuilding America - Turning the focused spending on rebuilding US infrastructure into revenue and profits.

Safety & Security – Targeted exposure to companies that provide goods and services primarily to the Defense and security sectors of the economy.

Space Economy – Companies that focus on the launch and operation of satellite networks.

The Strategies Behind Our Dividend Income Models

Monthly Dividend Model – Pretty much what the name says – this model invests in companies that pay monthly dividends to shareholders.

ETF Dividend Model – High-yielding ETFs that provide a range of exposures from domestic equities, international equities, emerging market equities, MLPS, and REITs.

ETF Enhanced Dividend Model – A group of high-yielding ETFs that utilize options to enhance yield through collecting option income.

Don’t be a stranger

Thanks for reading and if you have a suggestion for an article or book we should read, or a stream we should catch, email us at info@tematicaresearch.com. The same email works if you want to know more about our thematic and targeted exposure models listed below.