No Surprise, We’re Still in Data Dependent Mode

The Fed sees one rate cut ahead, but the market sees the door open for more

Note: The next edition of Thematic Signals will be published on June 24.

Market Recap

Equities continued to remain optimistic after a softer-than-expected CPI update (more below), so much so that even the market’s breadth proxy, the Russell 2000, was the top-performing broad index closing 1.62% higher. Technology exposure continues to make the difference among the Dow (-0.09%), S&P 500 (0.85%), and the Nasdaq Composite(1.53%), and indeed, the Technology Sector returned 2.21% as gains in Apple (AAPL) and Microsoft (MSFT) more than overcame similar percentage losses in Salesforce (CRM) and Accenture (ACN).

Consumer Discretionary (1.04%) followed as Lowe’s (LOW) and Home Depot (HD) had a strong day and were topped only by Tesla (TSLA) as news of Elon’s pay package approval led to the name to contribute just under 45% of the sector’s results.

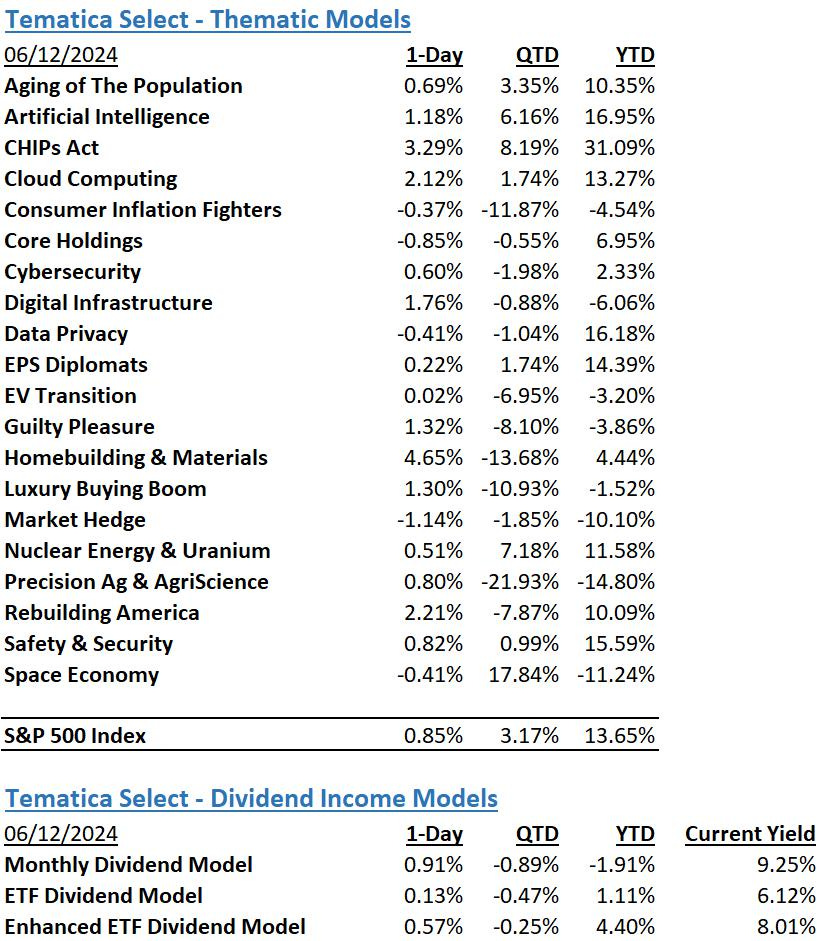

From a model perspective, Homebuilding & Materials won the day as that model’s constituents occupied 4 of the top ten leaderboard spots across all model constituents (see more below). As you can see in the table below, technology-focused models continued to show strength but sprinkled in the model leaders were Rebuilding America and Guilty Pleasure, indicating the market sentiment shifted to a more risk-on posture.

No Surprise, We’re Still in Data Dependent Mode

Despite the Fed’s economic projections now showing just one rate cut likely this year, the market powered ahead yesterday with the S&P 500 hitting a new all-time high. What began in response to the inflation progress shown in the May CPI report held following comments made during Fed Chair Powell’s press conference yesterday afternoon suggesting the Fed’s updated economic projections could be already outdated and a tad conservative. This has the market thinking that even though the Fed may see one rate cut this year, the door is open for two.

Once again, we are back in the camp of more good data is needed.

The Fed and investors will be examining today’s May PPI report to support the greater-than-expected downtick in sequential inflation data found in the May CPI report. Because the sequential May core CPI data was at 0.2% a few times in 2H 2024 only to rebound, it’s no surprise to us that Powell and the Fed Heads want to see “more good data”. They are concerned about getting head faked, hence Powell sharing yesterday’s report helped build confidence but did not give them the confidence they need to start cutting rates. If today’s May PPI report comes in below the expected reading of 0.5% MoM for both headline and core figures, it would be another step in the right direction.

Powell was also extremely clear the Fed isn’t leaning on any one data point or metric to begin a rate-cutting cycle. Rather the Fed will be looking at the “totality” of the data, something Powell shared will include inflation, job creation, and of course, the overall economy. Nothing new in our view, and it speaks the data hound in us.

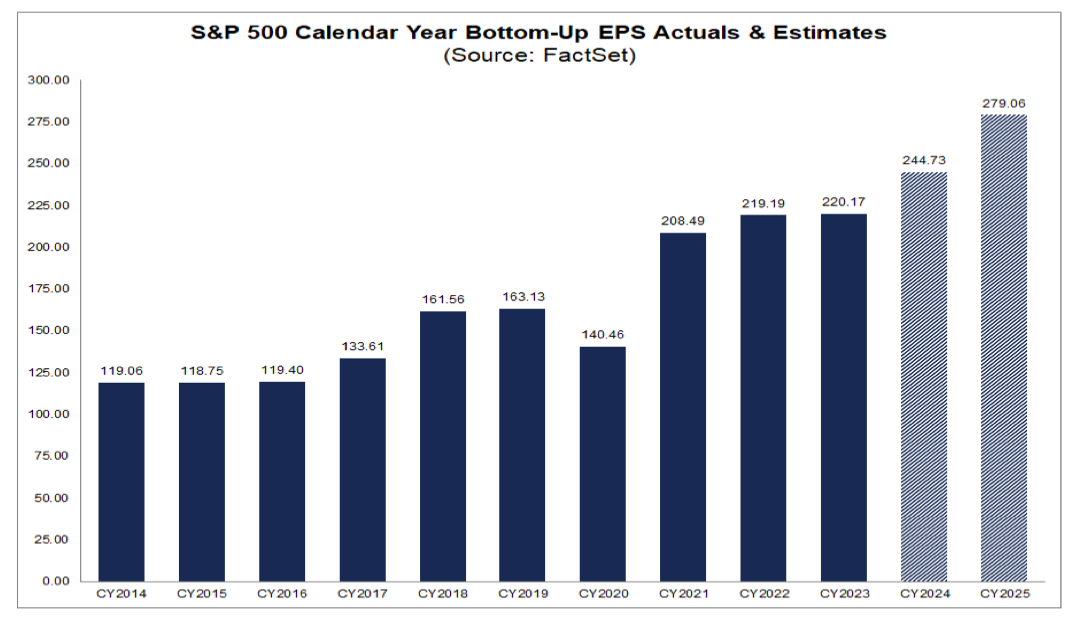

Looking at the calendar, the market will get a smattering of economic data for June, July, and August before the Fed’s September meeting. Should those upcoming data points show further progress as we saw in the May CPI report, they have the potential to re-ignite market expectations for more than one rate cut this year with additional cuts in 2025. That in turn could generate stronger expectations for more interest rate-sensitive parts of the economy, like the one captured by our Homebuilding & Materials model (more on that below), and help lift 2025 EPS expectations for the S&P 500. For those watching at home, the consensus 2025 EPS forecast published by FactSet already calls for the S&P 500 basket to grow its collected EPS by 14% to 2024.

Broadcom’s (AVGO) quarterly results last night should give further lift to our Artificial Intelligence, Cloud Computing, and Digital Infrastructure models. During its earnings call, Broadcom shared that its Networking revenue for the quarter soared 44% YoY to $3.8 billion “driven by strong demand from hyperscalers for both AI networking and custom accelerators.” Management at Broadcom expects the strength in AI to continue, and because of that, the company now sees its Networking revenue growing 40% YoY for its fiscal 2024, up from its prior guidance of 35%.

Model Musings

Consumer Inflation Fighters

“… 80% of American households have less cash available than they did in 2019, while credit card debt has reached a historic high. Meanwhile, a JP Morgan survey found that over 70% of low-income consumers are having a hard time making ends meet. Notably, middle-income households are also feeling pinched; 67% believe their income is falling behind the current cost of living… value messaging is proliferating everywhere right now – on TV, on social media, in brands’ apps, in consumers’ mailboxes.” Read more here

“Findings from the National Retail Federation’s NRF Retail Monitor announced Monday (June 10) showed that in May, consumer spending increased 1.35% relative to April, the highest month-to-month rise recorded in more than a year, and spending was up nearly 3% year over year… economic pressures continue to influence consumer behavior, leading to conservative spending patterns. Inflation in services and the lingering impacts of the pandemic on spending habits persist, prompting retailers to see consumers prioritizing essential expenditures and experiences over general merchandise and discretionary items.” Read more here

Cybersecurity

“Cybersecurity company Cylance confirmed the legitimacy of data being sold on a hacking forum, stating that it is old data stolen from a "third-party platform." The data allegedly includes a substantial amount of information, such as 34,000,000 customer and employee emails and personally identifiable information belonging to Cylance customers, partners, and employees.” Read more here

“Internal source code and data belonging to The New York Times was leaked on the 4chan message board after being stolen from the company's GitHub repositories in January 2024… The Times leak is the second one published to 4chan this week, with the first being a leak of 415MB of stolen internal documents for Disney's Club Penguin game. Sources exclusively told BleepingComputer that the Club Penguin leak was part of a more significant breach of Disney's Confluence server, where the threat actors stole 2.5 GB of internal corporate data.” Read more here

“On Monday (June 10), it was announced that a “significant volume of data” was stolen from at least 165 customers of multi-cloud data warehousing platform Snowflake, with the incident thought to be linked to earlier massive data breaches at Ticketmaster and Santander Bank; while the City of Cleveland suffered its own cyberattack on Sunday (June 9), forcing it to shut down its IT systems and citizen-facing services.” Read more here

Homebuilding & Materials

“Of about 1,400 resale agents nationwide surveyed by John Burns Research & Consulting, 99% said they’ve seen homes for sale that need repairs or updates, with two-thirds of agents saying listings showed deficiencies in at least four different areas, including outdated kitchens and bathrooms. The takeaway: Desperate homebuyers aren’t that desperate. Fixer-uppers can stay on the market longer and sometimes require discounts, with elevated prices and mortgage rates already straining the budgets of Americans looking to purchase a house.” Read more here

“The cost of owning a home in the US has increased 26% since 2020, as expenses including taxes, insurance and utilities all soared during a period of high inflation across the economy. The average annual outlay for owning and maintaining a typical single-family home — not including mortgage payments — totaled $18,118 in March, the personal finance website Bankrate found. That works out to $1,510 a month, roughly $300 more than four years earlier, when pandemic lockdowns began.” Read more here

Safety & Security

“In the U.K., Lidl last August said it became the first U.K. grocer to provide body-worn cameras to all associates in the region as part of efforts “to address the alarming rise of incidents facing retail workers every day.” Tesco also started providing body-worn cameras last fall to staff members after seeing physical assaults rise by a third in a year. U.K. bakery chain Greggs earlier this year gave associates body cameras after a rise in thefts and threats from customers…” Read more here

“In recent months, US supplies of 155mm shells have been drained by shipments to Ukraine and Washington’s support of Israel’s operations in the Gaza Strip. Black powder, the critical propellant for the shells, is also in short supply because the US produces little of it compared with the past. TNT, another basic component of ammunition, hasn’t been made in America since the 1980s—forcing the Pentagon to buy it from countries including Poland and Turkey… The Army is now playing a costly game of catchup. Congress has allocated $650 million for a TNT production facility that will take two years to build, according to Doug Bush, the Army’s top weapons buyer. ” Read more here

Space Economy

“Momentum is strong and aligns well with UBS’ preference for the industrials (XLI) sector, particularly aerospace and defense. “Space-based assets and defense technologies are increasingly front and center for governments, as rising geopolitical tensions underline the relationship between the space economy and security,” the LTI team said.” Read more here

The Strategies Behind Our Thematic Models

Aging of the Population - Capturing the demographic wave of the aging population and the changing demands it brings with it.

Artificial Intelligence – Software, chips, and related companies that facilitate the collection and analysis of large data sets and autonomous generation of solutions given non-machine language prompts.

CHIPs Act – Capturing the reshoring of the US semiconductor industry and the $52.7 billion poised to be spent on semiconductor manufacturing.

Cloud Computing – Companies that provide hardware and services that enhance the cloud computing experience for users, such as co-location, security, and edge computing.

Consumer Inflation Fighters - Companies poised to benefit as consumers stretch the disposable spending dollars they do have.

Core Holdings – Companies that reflect economic activity and are large enough to not get pushed around by day-to-day market trends. Low-beta, large-cap names able to better withstand economic turmoil.

Cybersecurity - Companies that focus on protecting against the penetration of digital networks and the theft, ransom, corruption or destruction of data.

Digital Infrastructure & Connectivity -The buildout and upgrading of our Networks, Data Storage Facilities, and Equipment.

Data Privacy & Digital Identity - Companies providing the tools and services that verify authorized users and safeguard personal data privacy.

EPS Diplomats - Profitable large capitalization companies proven to produce above-average EPS growth and provide investors with the benefit of multiple expansion.

EV Transition - Capturing the transition to EVs and related infrastructure from combustion engine vehicles.

Guilty Pleasure – Companies that produce/provide food and drink products that consumers tend to enjoy regardless of the economic environment and potential long-term health hazards associated with excessive consumption.

Homebuilding & Materials – Ranging from homebuilders to key building product companies that serve the housing market, this model looks to capture the rising demand for housing, one that should benefit as the Fed returns monetary policy to more normalized levels.

Luxury Buying Boom - Tapping into aspirational buying and affluent buyers amid rising global wealth.

Market Hedge Model – This basket of daily reset swap-based broad market inverse ETFs protects in the face of market pullbacks, overbought market technicals, and other drivers of market volatility.

Nuclear Energy & Uranium – Companies that either build and maintain nuclear power plants or are involved in the production of uranium.

Precision Ag & Agri Science – Companies that look to address shrinking arable land by helping maximize crop yields utilizing technology, science, or both.

Rebuilding America - Turning the focused spending on rebuilding US infrastructure into revenue and profits.

Safety & Security – Targeted exposure to companies that provide goods and services primarily to the Defense and security sectors of the economy.

Space Economy – Companies that focus on the launch and operation of satellite networks.

The Strategies Behind Our Dividend Income Models

Monthly Dividend Model – Pretty much what the name says – this model invests in companies that pay monthly dividends to shareholders.

ETF Dividend Model – High-yielding ETFs that provide a range of exposures from domestic equities, international equities, emerging market equities, MLPS, and REITs.

ETF Enhanced Dividend Model – A group of high-yielding ETFs that utilize options to enhance yield through collecting option income.

Don’t be a stranger

Thanks for reading and if you have a suggestion for an article or book we should read, or a stream we should catch, email us at info@tematicaresearch.com. The same email works if you want to know more about our thematic and targeted exposure models listed below.