Layoffs Heat Back Up, May PMI Data Points to Inflation Doing the Same

Bad news for the market, good news for these two model strategies

Market Recap

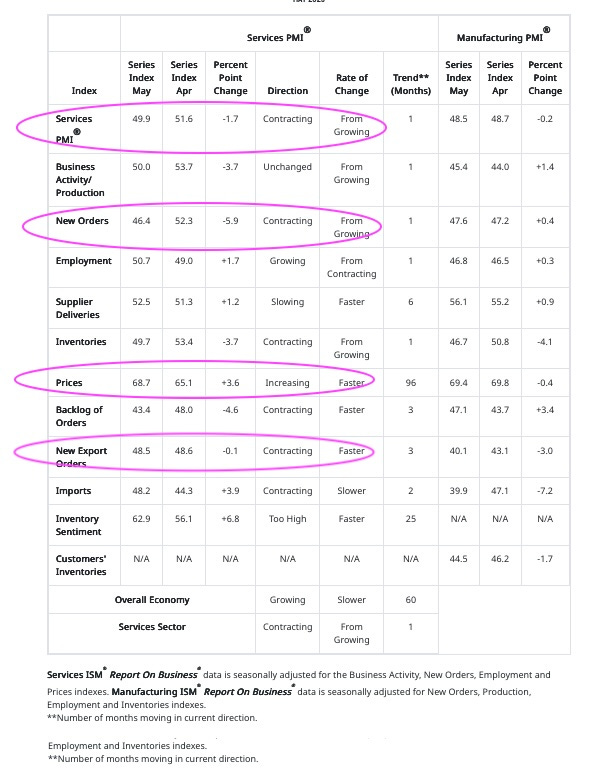

Despite the May ADP Jobs report (37K vs expected 130K) and May ISM Services PMI (49.9 vs expected 52.2) data that disappointed yesterday, broad equity indexes ended the day mixed. The Dow fell 0.22% but the S&P 500 eked out a 0.01% gain and the Nasdaq Composite closed 0.32% higher as Mag 7 names along with some technology and homebuilders helped balance out results. Small caps did not benefit from those names as the Russell 2000 dipped 0.21%. Sectors were mixed as well with Utilities and Energy leading the way lower falling 1.75% and 1.95%, respectively. The remaining sectors returned between 0.64% (Communication Services) and -0.70% (Consumer Staples).

Reports of higher-than-expected inventory levels helped push crude prices lower with West Texas Intermediate (WTI) falling 1.01% to $62.77/bbl. And Brent Light Sweet (BRENT) dropped 1.17% to $64.86/bbl. Gold ticked slightly higher to $3,372.30/oz and the Cboe Market Volatility Index (VIX) held relatively steady at 17.61.

The Tematica Select Model Suite saw mostly positive results with leadership coming from Space Economy (SPACE)and Homebuilding & Materials (HOMES). Laggards included Cybersecurity (CYBR) and Cloud Computing (CLOUD). With the steel and aluminum tariffs coming into play not to mention China’s rare earths export curbs, we’re paying attention to any impacts on Safety & Security (SAFE), EV Transition (TRANS), and to a certain extent, Nuclear Energy and Uranium (NUKE).

Layoffs Heat Back Up, May PMI Data Points to Inflation Doing the Same

Futures point to equities moving higher when the US stock market opens later this morning. In addition to the usual Thursday morning jobless claims data at 8:30 AM ET, this morning also brings Import and Export data for April at that time as well. In those Import/Export figures folks will be looking for confirmation of tariff-related stockpiling, something that could explain the figures found in the April PCE Price Index. However, when we look at the Price figures contained in ISM’s May Manufacturing & Services PMI data, we are not expecting market-friendly figures in next week’s May CPI and PPI reports.

Before we get to those weekly jobless claims and April Import/Export figures, at 7:30 AM ET, the Challenger Job Cuts report for May will be published at 7:30 AM ET and we suspect folks will be watching this closely following yesterday’s disappointing May ADP Employment Change Report, but also the latest Fed Beige Book published yesterday afternoon. The comment that stood out to us in that Beige Book was:

All Districts described lower labor demand, citing declining hours worked and overtime, hiring pauses, and staff reduction plans. Some Districts reported layoffs in certain sectors, but these layoffs were not pervasive.

Then this morning Procter & Gamble (PG) shared plans to cut 7,000 jobs, or roughly 15% of its nonmanufacturing workforce around the world, over the next two years. That follows word Microsoft (MSFT) will cut 6,000 across all levels, making it the company’s largest layoff since 2023. Both follow Intel’s (INTC) announcement to cut more than 20% of its staff in April.

The combination of higher prices in May per ISM’s data and renewed layoff headlines helps explain why Costco’s (COST) net sales for May rose 6.8% year over year with US comps adjusted for gas and foreign exchange up 5.5%. To us, that’s another confirmation point for our Cash-Strapped Consumer and Core Holdings models.

Turning to the Fed’s other mandate, maximum employment, S&P’s May Service PMI showed an upturn in hiring in the Services sector while ISM’s pointed to a rebound in hiring in that part of the economy as well. Granted at 50.7, the ISM Employment figure for May does not scream robust hiring but it’s likely to support a figure better than the disappointing 37,000 found in ADP’s May Employment Change Report.

Triangulating those figures, it’s hard to see how Friday’s Employment Report doesn’t deliver a May jobs figure below the 130,000 market consensus, which was already down from April’s 177,000 figure.

This is where things could get tricky for the market.

So long as job creation figures remain positive, and even if they dip into modest job losses, we’re likely to see the Fed remain focused on returning inflation back to its 2% target. Remember, several quarters ago, Fed Chair Powell signaled there could be some pain to get inflation down to that target. While that didn’t materialize in 2024, tariffs and the lack of trade deals so far mean we are on a different footing this year.

Should Friday’s May Employment Report disappoint, we could see the market move higher as the herd contemplates the Fed “doing more”. However, should next week’s CPI and PPI data confirm what we’re seeing in the ISM’s May PMI Price figures above and those from S&P, we could see the market gyrate as it re-thinks the number of expected Fed rate cuts.

All the more reason to tread carefully should the market move higher today and another one for why we’ll continue to heed the signals we collect each week. The next batch we’ll share with you will be out Saturday morning, so be sure to look for that missive!

The Strategies Behind Our Thematic Models

Aging of the Population - Capturing the demographic wave of the aging population and the changing demands it brings with it.

Artificial Intelligence – Software, chips, and related companies that facilitate the collection and analysis of large data sets and autonomous generation of solutions given non-machine language prompts.

Cash Strapped Consumers - Companies poised to benefit as consumers stretch the disposable spending dollars they do have.

CHIPs Act – Capturing the reshoring of the US semiconductor industry and the $52.7 billion poised to be spent on semiconductor manufacturing.

Cloud Computing – Companies that provide hardware and services that enhance the cloud computing experience for users, such as co-location, security, and edge computing.

Core Holdings – Companies that reflect economic activity and are large enough to not get pushed around by day-to-day market trends. Low-beta, large-cap names able to better withstand economic turmoil.

Cybersecurity - Companies that focus on protecting against the penetration of digital networks and the theft, ransom, corruption, or destruction of data.

Data Privacy & Digital Identity - Companies providing the tools and services that verify authorized users and safeguard personal data privacy.

Digital Infrastructure & Connectivity - Companies that are integral to the development and the buildout of the infrastructure that supports our increasingly connected world.

Digital Lifestyle - The companies behind our increasingly connected lives.

EPS Diplomats - Profitable large capitalization companies proven to produce above-average EPS growth and provide investors with the benefit of multiple expansion.

EV Transition - Capturing the transition to EVs and related infrastructure from combustion engine vehicles.

Guilty Pleasure – Companies that produce/provide food and drink products that consumers tend to enjoy regardless of the economic environment and potential long-term health hazards associated with excessive consumption.

Homebuilding & Materials – Ranging from homebuilders to key building product companies that serve the housing market, this model looks to capture the rising demand for housing, one that should benefit as the Fed returns monetary policy to more normalized levels.

Market Hedge Model – This basket of daily reset swap-based broad market inverse ETFs protects in the face of market pullbacks, overbought market technicals, and other drivers of market volatility.

Nuclear Energy & Uranium – Companies that either build and maintain nuclear power plants or are involved in the production of uranium.

Luxury Buying Boom - Tapping into aspirational buying and affluent buyers amid rising global wealth.

Rebuilding America - Turning the focused spending on rebuilding US infrastructure into revenue and profits.

Safety & Security – Targeted exposure to companies that provide goods and services primarily to the Defense and security sectors of the economy.

Space Economy – Companies that focus on the launch and operation of satellite networks.

The Strategies Behind Our Dividend Income Models

Monthly Dividend Model – Pretty much what the name indicates – this model invests in companies that pay monthly dividends to shareholders.

ETF Dividend Model – High-yielding ETFs that provide a range of exposures from domestic equities, international equities, emerging market equities, MLPS, and REITs.

ETF Enhanced Dividend Model – A group of high-yielding ETFs that utilize options to enhance yield through collecting option income.

Don’t be a stranger

Thanks for reading and if you have a suggestion for an article or book we should read, or a stream we should catch, email us at info@tematicaresearch.com. The same email works if you want to know more about our thematic and targeted exposure models listed above.