ISM and JOLTS Data, Fed Meeting Minutes Ahead

January 3, 2024

It looks like the recent whispers about Technology being overbought turned into an actual conversation yesterday as the sector traded off 2.62%. That’s a fair-sized number but when you consider the market capitalization represented in the sector it should be no surprise that broad market indexes suffered. Aside from the Dow which posted a 0.07% gain, the S&P 500 was down 0.57%, the Nasdaq Composite fell 1.63% and even the Russell 2000 gave up 0.70%. It wasn't all gloom and doom as Consumer Staples (1.12%) Utilities (1.45%) and Healthcare (1.76%) had a good day, but it was not enough to counter Technology and Communications Services, which also fell 0.56%.

ISM and JOLTS Data, Fed Meeting Minutes Ahead

US equity futures point to a lower open later this morning. Treasury yields, including those for the closely watched 10-year, are moving higher again this morning ahead of this morning’s December ISM Manufacturing PMI data and the November JOLTS Job Openings Report. Those back-to-back reports out at 10 AM ET will give the market a fresh look at the vector and velocity of the US economy. Following yesterday’s December Manufacturing PMI from S&P Global that found selling prices increased at the fastest rate since April, investors will be engrossed in findings from ISM on inflation and manufacturing activity. Even though the November JOLTS data is a bit of a rear-view perspective, the number of job openings reported will indicate the vitality of the jobs market and wage pressures.

Those morning reports will set the tone for the 2 PM ET publication of the Fed’s December policy meeting minutes. Exiting that meeting the Fed shared its updated economic projections that call for three rate hikes in 2024, half what the market is expecting. The meeting minutes will give us a behind-the-scenes look at that Fed rate cut conversation and could reveal what could spur the Fed to cut rates more aggressively or go at a slower pace. Recent Fed head comments have suggested the Fed may not begin cutting rates until 2H 2024. Should the meeting minutes reinforce that view and the December ISM report confirm slower-than-expected progress on inflation, investors are likely to question rate cut expectations that helped fuel the market’s rapid rise in November and December.

For more, be sure to read our Daily Markets column published each day by Nasdaq.

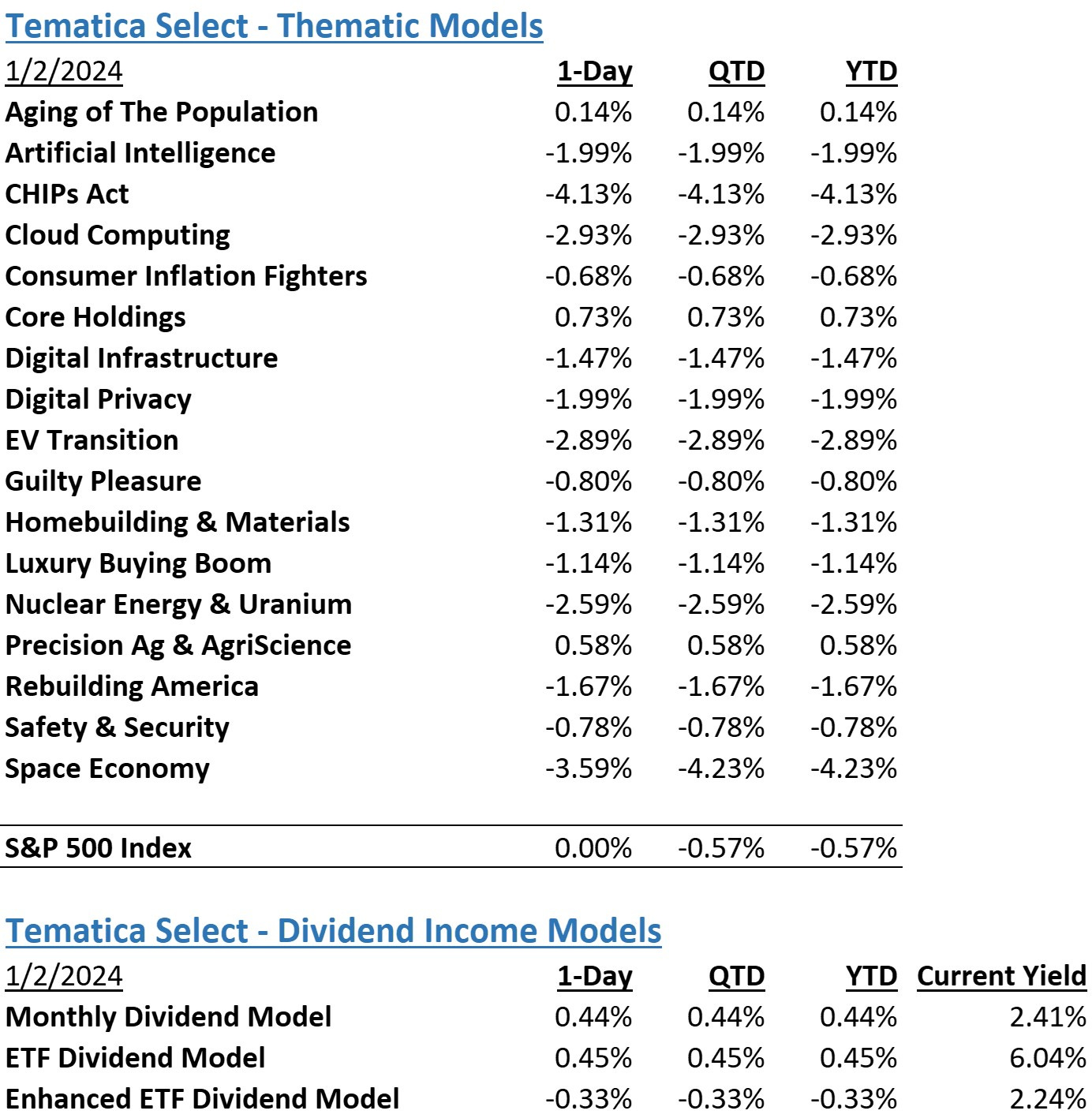

The strategies behind our Thematic Models:

Aging of the Population - Capturing the demographic wave of the aging population and the changing demands it brings with it.

Artificial Intelligence – Software, chips, and related companies that facilitate the collection and analysis of large data sets and autonomous generation of solutions given non-machine language prompts.

CHIPs Act – Capturing the reshoring of the US semiconductor industry and the $52.7 billion poised to be spent on semiconductor manufacturing.

Cloud Computing – Companies that provide hardware and services that enhance the cloud computing experience for users, such as co-location, security, and edge computing.

Consumer Inflation Fighters - Companies poised to benefit as consumers stretch the disposable spending dollars they do have.

Core Holdings – Companies that reflect economic activity and are large enough to not get pushed around by day-to-day market trends. Low-beta, large-cap names able to better withstand economic turmoil.

Digital Infrastructure & Connectivity -The buildout and upgrading of our Networks, Data Storage Facilities, and Equipment.

Data Privacy & Digital Identity - Companies providing the tools and services that verify authorized users and safeguard personal data privacy.

EV Transition - Capturing the transition to EVs and related infrastructure from combustion engine vehicles.

Guilty Pleasure – Companies that produce/provide food and drink products that consumers tend to enjoy regardless of the economic environment and potential long-term health hazards associated with excessive consumption.

Homebuilding & Materials – Ranging from homebuilders to key building product companies that serve the housing market, this model looks to capture the rising demand for housing, one that should benefit as the Fed returns monetary policy to more normalized levels.

Nuclear Energy & Uranium – Companies that either build and maintain nuclear power plants or are involved in the production of uranium.

Luxury Buying Boom - Tapping into aspirational buying and affluent buyers amid rising global wealth.

Precision Ag & Agri Science – Companies that look to address shrinking arable land by helping maximize crop yields utilizing technology, science, or both.

Rebuilding America - Turning the focused spending on rebuilding US infrastructure into revenue and profits.

Safety & Security – Targeted exposure to companies that provide goods and services primarily to the Defense and security sectors of the economy.

Space Economy – Companies that focus on the launch and operation of satellite networks.

The strategies behind our Dividend Income Models:

Monthly Dividend Model – Pretty much what the name says – this model invests in companies that pay monthly dividends to shareholders.

ETF Dividend Model – High-yielding ETFs that provide a range of exposures from domestic equities, international equities, emerging market equities, MLPS, and REITs.

ETF Enhanced Dividend Model – A group of high-yielding ETFs that utilize options to enhance yield through collecting option income.