February CPI - Market Sell Off or Buy the Dip?

The core CPI reading for February is expected to fall to 3.7% YoY but...

This morning gives us the latest inflation update (more below) and, as we have been discussing, it will provide another data point for market soothsayers to help predict the timing of the Fed’s next easing cycle. For the Fed, it will be one of the last pieces of data collected before they begin their March policy meeting next week. Several weeks ago, Fed Chair Powell telegraphed a March rate cut was off the table, but this will be one of those meetings after which the central bank shares its updated Economic Projections, including GDP and inflation forecasts for 2024. While both are expected to inch higher compared to their December figures, the degree of those revisions could push rate cut expectations, which have been slipping toward 3Q 2024 decidedly into that quarter.

Forecasts are calling for the top-line February CPI figure to come in even with January’s reading of 3.10% while the core figure (CPI ex-Food & Energy) is expected to have dropped slightly from 3.90% to 3.70%. To set the stage for the February data, the only Core item that dropped in the January YoY release was Used Cars & Trucks (-3.50%) while Shelter (6.00%), Tobacco and Smoking Products (7.40%), and Transportation Services(9.50%) led category gains. We’d also note data from AAA that shows the national average for gas rose $0.19 per gallon in February after falling between September and January.

Last night, the Fed funds Futures curve showed traders pricing in a roughly 55% chance of a 25 basis point cut at the June meeting and a combined 80% chance of at least a 25 basis point cut by July. Essentially, numbers coming in significantly lower than expectations could help move timing expectations forward, and evidence that inflation is running hotter will push those estimates out. The question for us is how traders will react to this February CPI findings vis-a-vis more profit-taking, as we’ve seen in recent days, or if it will it embolden them to once again “buy the dip”.

Early this morning, we learned the NFIB Small Business Optimism Index edged down to 89.4 in February, the lowest in nine months, from 89.9 in January, and below forecasts of 90.7. Twenty-three percent of small business owners reported that inflation was their single most important business problem in operating their business, up three points from last month, and replacing labor quality as the top problem.

For more, be sure to read our Daily Markets column published each day by Nasdaq.

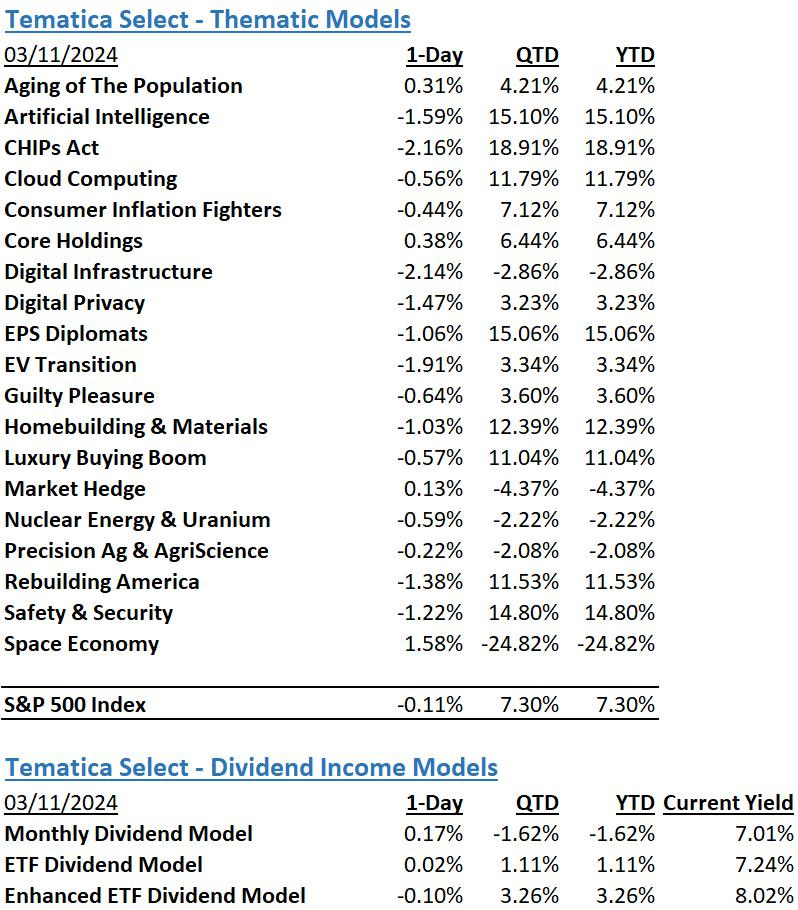

Model Musings

Data Privacy & Digital Identity

“Worldcoin, a digital ID cryptocurrency venture led by Sam Altman, CEO of OpenAI, has faced regulatory hurdles in Spain as the country’s data protection authority, AEPD, issues a temporary ban on its operations. The ban, effective for up to three months, follows complaints about alleged privacy violations related to the collection and processing of personal data.” Read more here

“This year might be a boon for biometric privacy legislation. The topic is heating up and lies at the intersection of four trends: increasing artificial intelligence (AI)-based threats, growing biometric usage by businesses, anticipated new state-level privacy legislation, and a new executive order issued by President Biden this week that includes biometric privacy protections.” Read more here

“Cybersecurity professionals are finding it more attractive to take their talents to the Dark Web and earn money working on the offensive side of cybercrime. This puts enterprises in a tough spot: cut into profit growth to keep cybersecurity skills from flowing to the highest bidder, or figure out how to defend their networks against those who know their weaknesses most intimately.” Read more here

Digital Infrastructure & Connectivity

“5G is expected to account for 51% of mobile connections in 2029, before hitting 56% the following year, according to the latest figures from GSMA Intelligence. 5G, which began commercialization in 2019, is the fastest-growing mobile technology, exceeding one billion connections in 2022 and climbing to 1.6 billion connections last year. It is projected to reach 5.5 billion by 2030. It took 4G nine years to hit 1.5 billion users. However, the adoption of 5G has encountered some bumps and the technology has failed to gain significant traction among enterprises. Industry players believe this situation will change with 5.5G or 5G-Advanced networks, which are expected to see commercial rollouts this year.” Read more here

The Strategies Behind Our Thematic Models

Aging of the Population - Capturing the demographic wave of the aging population and the changing demands it brings with it.

Artificial Intelligence – Software, chips, and related companies that facilitate the collection and analysis of large data sets and autonomous generation of solutions given non-machine language prompts.

CHIPs Act – Capturing the reshoring of the US semiconductor industry and the $52.7 billion poised to be spent on semiconductor manufacturing.

Cloud Computing – Companies that provide hardware and services that enhance the cloud computing experience for users, such as co-location, security, and edge computing.

Consumer Inflation Fighters - Companies poised to benefit as consumers stretch the disposable spending dollars they do have.

Core Holdings – Companies that reflect economic activity and are large enough to not get pushed around by day-to-day market trends. Low-beta, large-cap names able to better withstand economic turmoil.

Digital Infrastructure & Connectivity -The buildout and upgrading of our Networks, Data Storage Facilities, and Equipment.

Data Privacy & Digital Identity - Companies providing the tools and services that verify authorized users and safeguard personal data privacy.

EPS Diplomats - Profitable large capitalization companies proven to produce above-average EPS growth and provide investors with the benefit of multiple expansion.

EV Transition - Capturing the transition to EVs and related infrastructure from combustion engine vehicles.

Guilty Pleasure – Companies that produce/provide food and drink products that consumers tend to enjoy regardless of the economic environment and potential long-term health hazards associated with excessive consumption.

Homebuilding & Materials – Ranging from homebuilders to key building product companies that serve the housing market, this model looks to capture the rising demand for housing, one that should benefit as the Fed returns monetary policy to more normalized levels.

Market Hedge Model – This basket of daily reset swap-based broad market inverse ETFs protects in the face of market pullbacks, overbought market technicals, and other drivers of market volatility.

Luxury Buying Boom - Tapping into aspirational buying and affluent buyers amid rising global wealth.

Market Hedge Model – This basket of daily reset swap-based broad market inverse ETFs protects in the face of market pullbacks, overbought market technicals, and other drivers of market volatility.

Nuclear Energy & Uranium – Companies that either build and maintain nuclear power plants or are involved in the production of uranium.

Precision Ag & Agri Science – Companies that look to address shrinking arable land by helping maximize crop yields utilizing technology, science, or both.

Rebuilding America - Turning the focused spending on rebuilding US infrastructure into revenue and profits.

Safety & Security – Targeted exposure to companies that provide goods and services primarily to the Defense and security sectors of the economy.

Space Economy – Companies that focus on the launch and operation of satellite networks.

The strategies behind our Dividend Income Models:

Monthly Dividend Model – Pretty much what the name says – this model invests in companies that pay monthly dividends to shareholders.

ETF Dividend Model – High-yielding ETFs that provide a range of exposures from domestic equities, international equities, emerging market equities, MLPS, and REITs.

ETF Enhanced Dividend Model – A group of high-yielding ETFs that utilize options to enhance yield through collecting option income.

Don’t be a stranger

Thanks for reading and if you have a suggestion for an article or book we should read, or a stream we should catch, email us at info@tematicaresearch.com. The same email works if you want to know more about our thematic and targeted exposure models listed below.