Balancing Maximum Employment & Price Stability

Fed likes what it's seeing in labor markets and continued moderation in inflation but wants more time to ensure trends are entrenched

On Tuesday, we talked about how this week was going to be giving us a closer look into the state of the consumer. We have gotten a few data points since then and they seem to point to pockets of what makes up “the consumer” are under pressure and starting to pull back. The evidence here comes in the form of results from companies like Starbucks (SBUX) reporting same-store sales down 2% in the US and 7% internationally and of course Monday’s McDonald’s (MCD) double miss on lower volumes as well. While these are massive companies, both here and overseas, it is speculated that some of these declines may be in part due to boycott efforts against both companies over their position(s) on the ongoing Israel/Hamas conflict. Outside of these cases, we did see results from Mastercard (MA) that continue to point to strength in consumer spending, results like those from Stanley Black & Decker (SWK) CEO that, despite revenues shrinking 3% as compared to Q2 2023 showed gross margins rising 6% over the same period. Similarly, PayPal (PYPL) came out swinging, beating EPS estimates by $0.20 and outpacing revenue estimates on transaction margin dollar growth of 3% compared to the previous quarter. Additionally, SOFI Technologies (SOFI) posted an earnings beat attributed to improved Lending and Financial Services while also seeing a modest decline in personal loan delinquencies.

Today we’ll have Amazon (AMZN) and Apple (AAPL) report Q2 earnings. Given this backdrop of a stressed but still spending consumer despite recent labor market adjustments it doesn’t look to us that either of these results are going to be causing any major shift in sentiment. Having said that, we are interested to see what effect China’s response to US sanctions will have had on Q2 results. Overall, we expect to see more business as usual from markets, but to quote chair Powell from yesterday’s post-announcement presser, “Certainty is not a word that we have in our business.”

Speaking of yesterday’s meeting essentially, the Fed likes what it’s seeing on inflation, labor markets, and economic growth but wants to see more data confirming that these trends are entrenched. From the Q&A session, takeaway points include the above quote, the reminder that the Fed is, “data dependent but not data point dependent” and Powell stating that the Fed is getting closer to the point of considering a rate cut, but they’re not there yet. Regardless of Chair Powell’s comments analysts were not deterred from trumpeting that the next easing cycle is upon us and will definitively start in September. Looks like we’re back to risk-on.

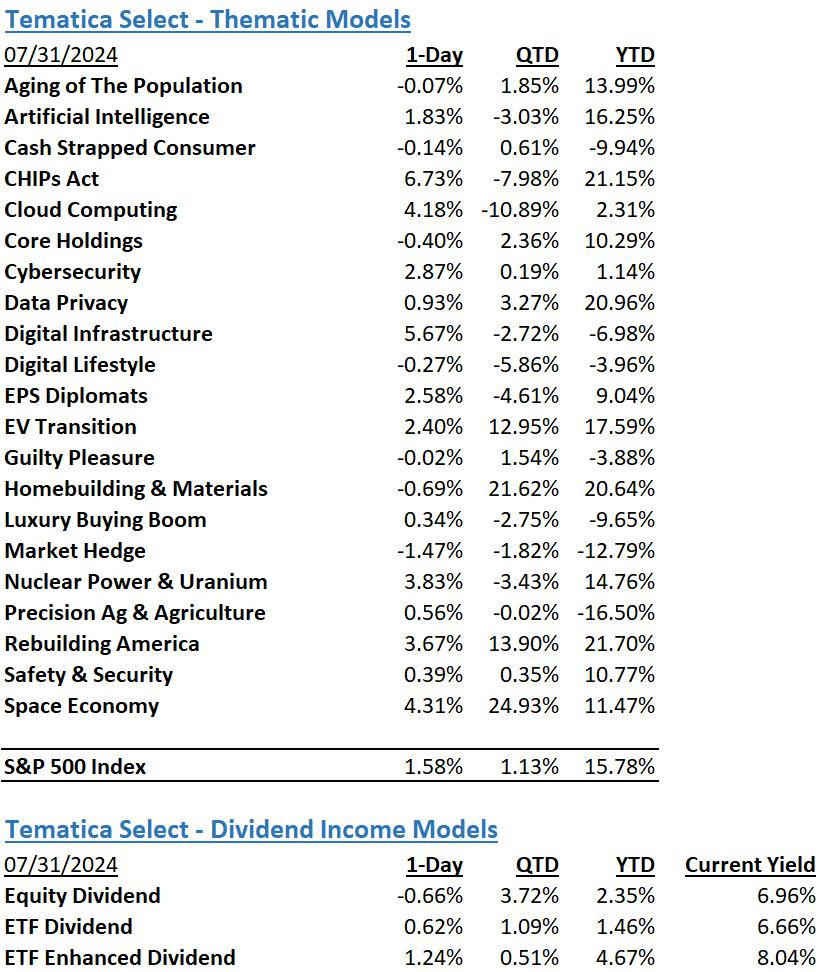

Model Musings

Cybersecurity

“Last week, one of the largest IT outages in history disrupted businesses and governments around the world.

The incident, which affected 8.5 million Microsoft Windows devices, led to widespread disruptions of airlines, banks, broadcasters, healthcare providers, retail payment terminals and cash machines globally. The cost of the outage is estimated to top $1 billion.” Read More Here

Optiv 2024 Cybersecurity Threat and Risk Management Report: “The purpose of this research is to learn the extent of the cybersecurity threats facing organizations and the steps being taken to manage the risks of potential data breaches and cyberattacks. Ponemon Institute surveyed 650 IT and cybersecurity practitioners in the US who are knowledgeable about their organizations’ approach to threat and risk management practices.” Read More Here

“UK businesses encountered a new cyberattack online every 44 seconds in the second quarter of 2024. Although most online attacks were detected and blocked at a network level or by company firewalls, there were five percent more this year than in the same period of 2023, with companies connected to the internet encountering 180,714 attacks each, on average, between April and June.” Read More Here

“An unexpected usage spike resulted in Azure Front Door (AFD) and Azure Content Delivery Network (CDN) components performing below acceptable thresholds, leading to intermittent errors, timeout, and latency spikes. While the initial trigger event was a Distributed Denial-of-Service (DDoS) attack, which activated our DDoS protection mechanisms, initial investigations suggest that an error in the implementation of our defenses amplified the impact of the attack rather than mitigating it.” Read More Here

Digital Infrastructure

“The Broadband Equity, Access, and Deployment (BEAD) program was created by a US law that requires Internet providers receiving federal funds to offer at least one "low-cost broadband service option for eligible subscribers." The Biden administration says it is merely enforcing that legal requirement, but a July 23 letter sent by over 30 broadband industry trade groups claims that the administration is illegally regulating broadband prices.” Read More Here

Space Economy

“The global space economy totaled $570 billion in 2023, 7.4% higher than 2022’s revised sum of $531 billion. This growth is consistent with the industry’s five-year compound annual growth rate (CAGR) of 7.3% and is nearly double the size of the space economy a decade ago.” Read More Here

The Strategies Behind Our Thematic Models

Aging of the Population - Capturing the demographic wave of the aging population and the changing demands it brings with it.

Artificial Intelligence – Software, chips, and related companies that facilitate the collection and analysis of large data sets and autonomous generation of solutions given non-machine language prompts.

Cash Strapped Consumer - Companies poised to benefit as consumers stretch the disposable spending dollars they do have.CHIPs Act – Capturing the reshoring of the US semiconductor industry and the $52.7 billion poised to be spent on semiconductor manufacturing.

Cloud Computing – Companies that provide hardware and services that enhance the cloud computing experience for users, such as co-location, security, and edge computing.

Core Holdings – Companies that reflect economic activity and are large enough to not get pushed around by day-to-day market trends. Low-beta, large-cap names able to better withstand economic turmoil.

Cybersecurity - Companies that focus on protecting against the penetration of digital networks and the theft, ransom, corruption or destruction of data.

Digital Infrastructure & Connectivity -The buildout and upgrading of our Networks, Data Storage Facilities, and Equipment.

Digital Lifestyle - The companies behind our increasingly connected lives.

Data Privacy & Digital Identity - Companies providing the tools and services that verify authorized users and safeguard personal data privacy.

EPS Diplomats - Profitable large capitalization companies proven to produce above-average EPS growth and provide investors with the benefit of multiple expansion.

EV Transition - Capturing the transition to EVs and related infrastructure from combustion engine vehicles.

Guilty Pleasure – Companies that produce/provide food and drink products that consumers tend to enjoy regardless of the economic environment and potential long-term health hazards associated with excessive consumption.

Homebuilding & Materials – Ranging from homebuilders to key building product companies that serve the housing market, this model looks to capture the rising demand for housing, one that should benefit as the Fed returns monetary policy to more normalized levels.

Luxury Buying Boom - Tapping into aspirational buying and affluent buyers amid rising global wealth.

Market Hedge Model – This basket of daily reset swap-based broad market inverse ETFs protects in the face of market pullbacks, overbought market technicals, and other drivers of market volatility.

Nuclear Energy & Uranium – Companies that either build and maintain nuclear power plants or are involved in the production of uranium.

Precision Ag & Agri Science – Companies that look to address shrinking arable land by helping maximize crop yields utilizing technology, science, or both.

Rebuilding America - Turning the focused spending on rebuilding US infrastructure into revenue and profits.

Safety & Security – Targeted exposure to companies that provide goods and services primarily to the Defense and security sectors of the economy.

Space Economy – Companies that focus on the launch and operation of satellite networks.

The Strategies Behind Our Dividend Income Models

Monthly Dividend Model – Pretty much what the name says – this model invests in companies that pay monthly dividends to shareholders.

ETF Dividend Model – High-yielding ETFs that provide a range of exposures from domestic equities, international equities, emerging market equities, MLPS, and REITs.

ETF Enhanced Dividend Model – A group of high-yielding ETFs that utilize options to enhance yield through collecting option income.

Don’t be a stranger

Thanks for reading and if you have a suggestion for an article or book we should read, or a stream we should catch, email us at info@tematicaresearch.com. The same email works if you want to know more about our thematic and targeted exposure models listed below.